Note: I am travelling until mid-May. Postings will be irregular.

Note: I am travelling until mid-May. Postings will be irregular.

US Employers Add 177,000 Jobs, Solid Pace in Face of Uncertainty

Nonfarm payrolls increased 177,000 last month after the prior two months’ advances were revised lower, according to Bureau of Labor Statistics data out Friday. The unemployment rate was unchanged at 4.2%.

The report suggests the labor market continues to cool gradually, a sign that businesses facing heightened uncertainty around tariffs and turmoil in financial markets didn’t significantly alter their hiring plans. Most economists anticipate the brunt of the impact from punishing levies will be seen in coming months. (…)

Payroll gains were broad based, led by an advance in health care. Transportation and warehousing employment rose by the most since December, suggesting a surge in imports and activity boosted demand for labor as businesses rushed to get ahead of tariffs. Manufacturing, meanwhile, shed jobs as the sector saw the steepest contraction in output last month since 2020.

The federal government cut jobs for a third month — the longest such streak since 2022 — reflecting efforts by the Elon Musk-led Department of Government Efficiency to downsize the federal workforce and reduce government spending.

The government leads all US industries in terms of layoffs announced so far in 2025, with the vast majority of the about 282,000 cuts being attributed to DOGE actions, outplacement firm Challenger, Gray & Christmas said in a report Thursday. Economists contend at least half a million US jobs could be on the line as federal spending cuts spread to contractors, universities and others who rely on government funding.

The participation rate — the share of the population that is working or looking for work — ticked up to 62.6% in April. The rate for those between the ages of 25 and 54, known as prime-age workers, rose to the highest level in seven months.

(…) The report showed average hourly earnings rose 0.2% last month, marking a deceleration from March. From a year earlier, they rose 3.8%. (…)

Cynics are saying the “R” word is not recession but rather resilience. But the early cracks are showing up:

- The prior two months jobs were revised down 58k.

- Employment growth was 0.1% MoM and has averaged +1.1% annualized in the first 4 months of the year.

- Wages rose 2.0% a.r. in April, down from 2.9% in February-March and 4.0% in the second half of 2024.

Q2 is thus off to a slow start from an aggregate income viewpoint, right when tariffs are about to hit.

The JOLTS report last week showed March job openings back to the Indeed Job Postings index but the latter keeps declining through April 25. Labor demand is clearly slowing and so are wages.

KKR:

This was a strong headline report. However, sector data suggests we are still not seeing the full impact of either DOGE cuts or tariffs on employment. Consider that Education/Healthcare employment still has not slowed (+70k, right around its last six months average) while Government added +10k jobs on net (still in positive territory, thanks to state and local hiring even as Federal jobs shed -9k workers).

Meanwhile, Construction and Manufacturing added a net +11k jobs, which is exactly in line with the last six months average, and we see some signs that prebuying activity ahead of tariffs drove labor demand (e.g., Trade/Transport ex-retail was +34k, up from

+3k last month), which we do not view as sustainable. (…)The good news is that we see fewer signs of stagflation in the labor market, which should give the Fed more breathing room heading into next week’s CPI report. Average hourly earnings have slowed to +3.2% on a 3-month annualized basis, down from the low-mid four percent range in late 2024.

Meanwhile, unemployment is stuck at 4.2% for the second month in a row, +30 basis points above where it was a year ago but still too low to force the Fed into a more dovish posture.

Importantly, oil prices at $58 are down 27% from January levels and 30% from their July 2024 level, boosting discretionary income and, thanks to slowing wages, critically keeping a lid on services inflation while we await tariff inflation on goods.

The surprise could be that slower than feared overall inflation keeps consumers and businesses afloat and provide room for rate cuts if and when needed. Let’s not forget that the U.S. economy is mainly services (although the S&P 500 is mainly goods).

Trump Budget Seeks 23% Domestic Cut, Omits Economic Forecast

The president’s budget calls for $557 billion in non-defense spending next year, which represents a cut of $163 billion from current levels. National security funding would increase to $1.01 trillion, a 13% increase from the previous year. Any final spending plan for regular agency budgets will need some Democratic support to pass the Senate, one of the few opportunities the minority party has to exert some leverage while Republicans have unified control over the federal government.

Known as the skinny budget because of its lack of detail, the document is a new president’s first opportunity to outline his vision for the size and scope of the federal government.

But Trump’s version was even thinner than usual, omitting baseline economic and interest-rate projections, which are typically a feature of budget proposals submitted by the White House in prior administrations.

There was also no set of forecasts for government debt, deficits or tax revenue in the document. Also excluded: any projections related to entitlement programs — headlined by Social Security and Medicaid — which are large drivers of overall federal spending.

Those details will be made later in the year, after Republicans work through the details of a giant tax cut bill set to move through Congress in the coming months, a senior Office of Management and Budget official told reporters on Friday. That legislation is slated to add trillions to deficits. (…)

On the domestic side, Trump is proposing a 22.6% cut in spending for the 2025 fiscal year. The proposal would slash environmental and renewable energy programs and calls on lawmakers to cancel $15 billion in former President Joe Biden’s signature infrastructure law for green energy funding.

The White House previewed the budget with a series of talking points that highlighted Trump’s use the spending plan as social policy document. Proposed reductions in early childhood education, housing, science and foreign aid were branded as “Cuts to Woke.” The elimination of $3.5 billion in refugee assistance came under the heading “Defunding the Open Border.” Climate, environment and renewable energy programs would be slashed on the premise of “Ending the Green New Scam.”

A senior OMB official described the plan as a paradigm shift, with historic commitments to defense and homeland security secured through the tax package which Democrats are powerless to block, unlike in Trump’s first term.

Agencies getting some of the biggest proposed cuts include a 26% reduction to the Department of Health and Human Services, 33% to the Small Business Administration, 44% to Housing and Urban Development, 54% to the Environmental Protection Agency and 56% to the National Science Foundation. (…)

The budget illustrates that DOGE’s effort would not ultimately result in significant deficit savings. It proposes to hold all non-emergency discretionary funding flat at $1.613 trillion when almost $120 billion in defense funding is added via Trump’s tax bill. Overall cuts are attributed to emergency funding, such as that for natural disasters, which can easily increase in the wake of storms, flood and fires.

The Trump plan also illustrates the limits of savings from cutting agency operating budgets and personnel in a federal budget dominated by giant entitlement programs as federal debt payments increase from interest rates that are notably higher now than in the years prior to the pandemic. (…)

The budget would cut 10% from last year’s level of discretionary spending — things the government does excluding mandatory programs like Social Security and Medicare.

- But the White House wants to increase spending for border security and defense, so the bulk of the cuts are on non-defense programs, like health care, education, and housing.

The cuts would bring non-defense discretionary spending to its lowest level in modern history — less than 2% of GDP, compared to an average 3.1% over the past 40 years, per an analysis from Bobby Kogan, a senior director of federal budget policy at the liberal Center for American Progress.

“They are calling for something that is extreme, objectively, and even by Trump standards,” adds Kogan, who worked at the Office of Management and Budget during the Biden administration. (…)

A president’s budget is just a wish list; Congress doesn’t simply put it through.

This is just a partial proposal, it doesn’t discuss Trump’s plans for tax breaks. Some of those, like no taxes on tips, could theoretically help lower earners.

It also doesn’t cover Medicaid, the federal health insurance program for lower-income Americans. That’s reportedly on House Republicans’ chopping block.

GM Cuts Workers at Canada Truck Plant, Citing Trade Turmoil

GO WITH THE FLOWS?

- Based on flows, retail confidence is still very high while the pros are very cautious.

Source: @WallStJesus

- With the US dollar heading into bear market and political risk weighing heavily, foreigners have had a clear change in heart on US assets with net outflows from US bond funds, and a sharp drop in demand for US stocks. (Callum Thomas)

Source: @lisaabramowicz1

TRUE EXCEPTIONALISM

Goldman Sachs’ excellent and essential annual ROE analysis:

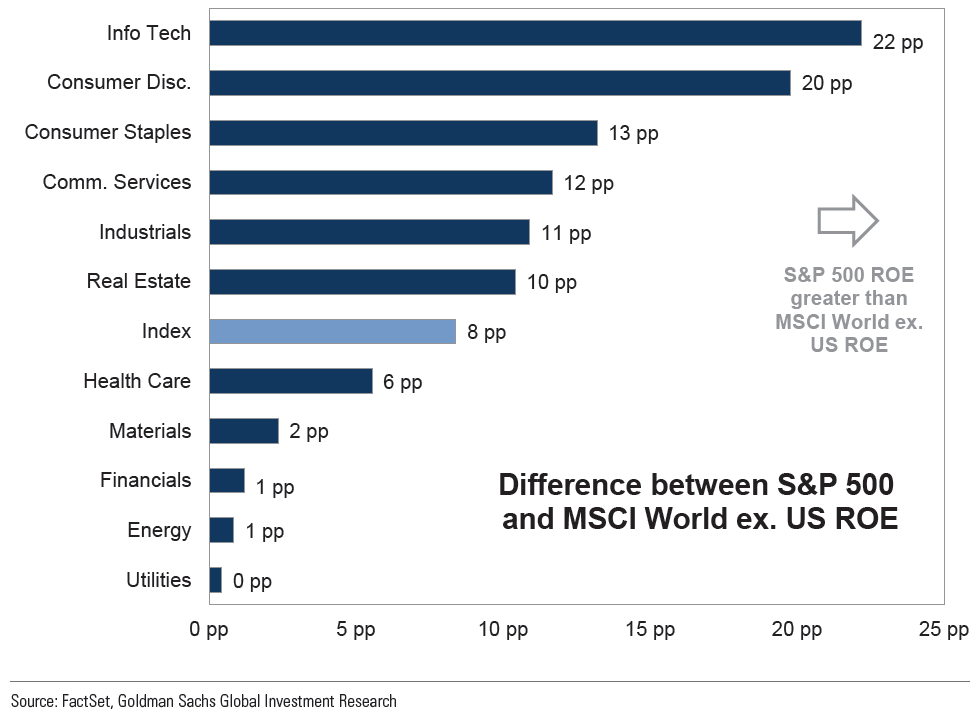

The S&P 500 index ROE is 8 pp greater than the rest of the developed world (21% vs. 12%) and helps explain the US stock market’s valuation premium vs. the MSCI World ex. US index.

The aggregate ROE gap now ranks in the 92nd percentile and S&P 500 ROE is greater than other DM equity markets in each of the 11 sectors.

While the S&P 500 currently trades at a 2.4x greater Price/Book (P/B) multiple vs. the MSCI World ex. US (4.2x vs. 1.8x), valuations across regions and sectors appear consistent with expected profitability.

The ROE gap is largest in Info Tech (22 pp) and Consumer Discretionary (20 pp), but the gap extends to every sector in the S&P 500.

The primary drivers of the ROE gap between the US and other DM markets are higher EBIT margins (17% vs. 15%) and greater asset turnover (38% vs. 17%).

The primary drivers of the ROE gap between the US and the rest of world are higher EBIT margins and higher asset turnover.

EBIT margins are higher in 6 out of 9 sectors (excluding Financials and Real Estate) in the S&P 500 compared to the MSCI World ex. US. The gap is largest within Info Tech (16 pp), Utilities (9 pp), and Comm Services (8 pp). The Health Care sector is the most notable exception, where MSCI World ex. US EBIT margins stand at 23% compared with the S&P 500 sector at 10%.

Looking ahead, the S&P 500 will likely maintain its superior ROE relative to other DM equity markets, but a substantial further widening of the ROE gap appears challenging given the headwinds to profit margins. In addition, the tailwind to S&P 500 ROE from the Magnificent 7 appears to be slowing. As a result, a substantial ROE-driven expansion in the valuation gap between the US and MSCI ex. US appears unlikely.

Hmmm… Goldman assumes that a 16pp jump in the U.S. tariff rate to 19% combined with sharply decelerating GDP growth “will lead to roughly flat profit margins in 2025.”

Much slower revenue growth and a quick, sudden huge cost increase is very unlikely to leave margins unscathed. In fact, Goldman adds “the US-led nature of this economic shock could create a larger risk to US profitability.”

Also,

The tailwind to S&P 500 ROE from the Magnificent 7 appears to be fading as well. The Mag 7 composes 31% of the total index market cap and 26% of S&P 500 earnings. Mag 7 ROE expanded from 33% in 2022 to 39% in 2024, boosting the aggregate S&P 500 ROE despite S&P 493 ROE declining from 20% to 18% during this time. However, looking ahead, consensus expects Mag 7 ROE will contract to 35% in 2025 and 31% in 2026, primarily driven by a decrease in asset turnover and leverage, while ROE for the S&P 493 will expand slightly to 19%.

The S&P 493 ROE declined in a strong economy in 2024. I doubt they could expand in 2025, even stay flat.

Of course, we are still in the dark on actual tariffs and potential retaliation but we can safely assume that 2025-26 will be much different than 2024 for growth and business costs.

EARNINGS WATCH

357 companies in the S&P 500 Index have reported earnings for Q1 2025. Of these companies, 74.2% reported earnings above analyst expectations and 20.4% reported earnings below analyst expectations. In a typical quarter (since 1994), 67% of companies beat estimates and 20% miss estimates. Over the past four quarters, 77% of companies beat the estimates and 17% missed estimates.

In aggregate, companies are reporting earnings that are 7.0% above estimates, which compares to a long-term (since 1994) average surprise factor of 4.3% and the average surprise factor over the prior four quarters of 6.8%.

Of these companies, 61.2% reported revenue above analyst expectations and 38.8% reported revenue below analyst expectations. In a typical quarter (since 2002), 62% of companies beat estimates and 38% miss estimates. Over the past four quarters, 62% of

companies beat the estimates and 38% missed estimates.In aggregate, companies are reporting revenues that are 0.9% above estimates, which compares to a long-term (since 2002) average surprise factor of 1.3% and the average surprise factor over the prior four quarters of 1.2%.

The estimated earnings growth rate for the S&P 500 for 25Q1 is 13.6%. If the energy sector is excluded, the growth rate improves to 15.7%.

The estimated revenue growth rate for the S&P 500 for 25Q1 is 4.6%. If the energy sector is excluded, the growth rate improves to 5.1%.

The estimated earnings growth rate for the S&P 500 for 25Q2 is 6.9%. If the energy sector is excluded, the growth rate improves to 8.6%.

Remarkably, pre-announcements are not terribly negative at this time:

But GS explains:

Forward guidance trends reflect an elevated level of uncertainty among corporates. So far this reporting season, a slightly lower proportion of companies are offering EPS guidance than average. Among those that have continued to guide, an above-average share have maintained previous guidance in place. We view this dynamic partly as a reflection of corporate’s hesitancy to shift guidance due to uncertainty around tariff policy.

Management commentary has been focused on the risk of recession and the potential impact of tariffs. 24% of the 357 S&P 500 companies reporting so far have mentioned the word “recession” on their conference calls, compared with just 2% last quarter. We highlight selected quotes from managements discussing recession risk and discussing the potential impact of tariffs on their businesses.

Of companies that have provided FY1 guidance, an above-average share of companies have maintained previous FY1 guidance in place. We view this dynamic partly as a reflection of corporate’s hesitancy to shift guidance due to uncertainty around tariff policy. For example, some companies noted in their earnings calls that their most recent guidance does not incorporate the impact of tariffs.

Q2 estimates have come down, but are still up:

So are full year estimates:

Trailing EPS are now $250.67, a $5 jump from last week. Full year 2025e: $264.69. Forward EPS: $271.54.

But GS notes that sales and capex revisions are sharply down in recent weeks, reflecting corporate uncertainty and cautiousness:

A tally of annual tariff costs is now $4.4B for 9 companies that have provided cost estimates. Proctor and Gamble, a consumer staples company, said: “The $1 billion to $1.5 billion before tax is the impact that we are estimating based on what we know today. That means the tariff rates that have been announced and enacted both in the US and in all other markets in response to the US tariffs. Exactly as you say, that’s about 3% of cost of goods sold about 140 to 180 basis points margin impact.”

Some quotes gleaned here and there:

- The fragile balance that underpins the global equipment supply chain has collapsed. Ocean container bookings have plummeted by 64 percent, which means 64 percent of our business has vanished overnight. Without incoming containers, there is nothing to reload, nothing to export and no way to keep our trucks moving. This loss of freight in the market will bleed into every area of transportation. I have already had to make the heartbreaking decision to lay off one third of my staff. Any further cuts would cripple our ability to operate at even the most basic level. At this point, we are staring down the very real possibility of shutting down entirely. Ten years of fighting to keep a company alive and people employed through a global pandemic, the freight recession of 2023–24, and now this.

- The risk we face now is far greater and less understood than what we saw during the COVID shutdown. Consumers and businesses will limit investment and orders until there is some sense of stability, and we have already experienced this with smaller orders and delayed orders. It’s chaos right now.

Trump Calls for 100% Tariff on Movies Made Overseas The president called the use of incentives by foreign countries to draw filmmakers and studios away from the U.S. a national-security threat

President Trump has found the next industry he wants to bring back to the U.S. with tariffs: Hollywood.

Trump authorized a 100% tariff on films produced overseas, he said in a Truth Social post Sunday. He called it a response to tax incentives that have lured a substantial number of Hollywood productions outside the U.S.

Films made by American studios are often shot in the United Kingdom and Canada, including this year’s highest-grossing film, “A Minecraft Movie.”

“The Movie Industry in America is DYING a very fast death,” the president wrote. He called international filmmaking incentives “a concerted effort by other Nations and, therefore, a National Security threat. It is, in addition to everything else, messaging and propaganda!”

Hollywood studio executives scrambled Sunday night to determine what the announcement would mean for their business. Executives said they were given no prior warning about the tariff plan and no information about how it might work.

It is unclear how such a tariff would work because movies aren’t physical goods that move through ports like most items subject to tariffs. The Trump administration would need to determine how to value a movie in order to apply the tariffs, as well as what the threshold would be to classify it as an import.

If other countries imposed reciprocal tariffs, it could devastate Hollywood studios, since most big-budget event films earn the majority of their revenue overseas. (…)

The U.S. movie industry had a $15.3 billion trade surplus in 2023 and generated a positive balance of trade with every major foreign market, according to a report from the Motion Picture Association, an industry trade group.

Some of summer’s biggest productions including “Mission: Impossible – The Final Reckoning” and “Jurassic World Rebirth” were made primarily or entirely outside the U.S.

London in particular has become a thriving hub for Hollywood productions, because of its tax incentives, extensive infrastructure including large soundstages, and English-speaking crews. Disney’s Marvel Studios is shooting a pair of upcoming Avengers sequels there.

The total amount of money spent last year on film and television productions in the U.S. with budgets of more than $40 million fell 26% from two years earlier, according to research firm ProdPro. It rose during that period in the U.K. and Canada, though neither market has yet caught up to the U.S. (…)

AI CORNER

Performance scores of top US and Chinese AI models:

Source: J.P. Morgan Asset Management

{kind=link}